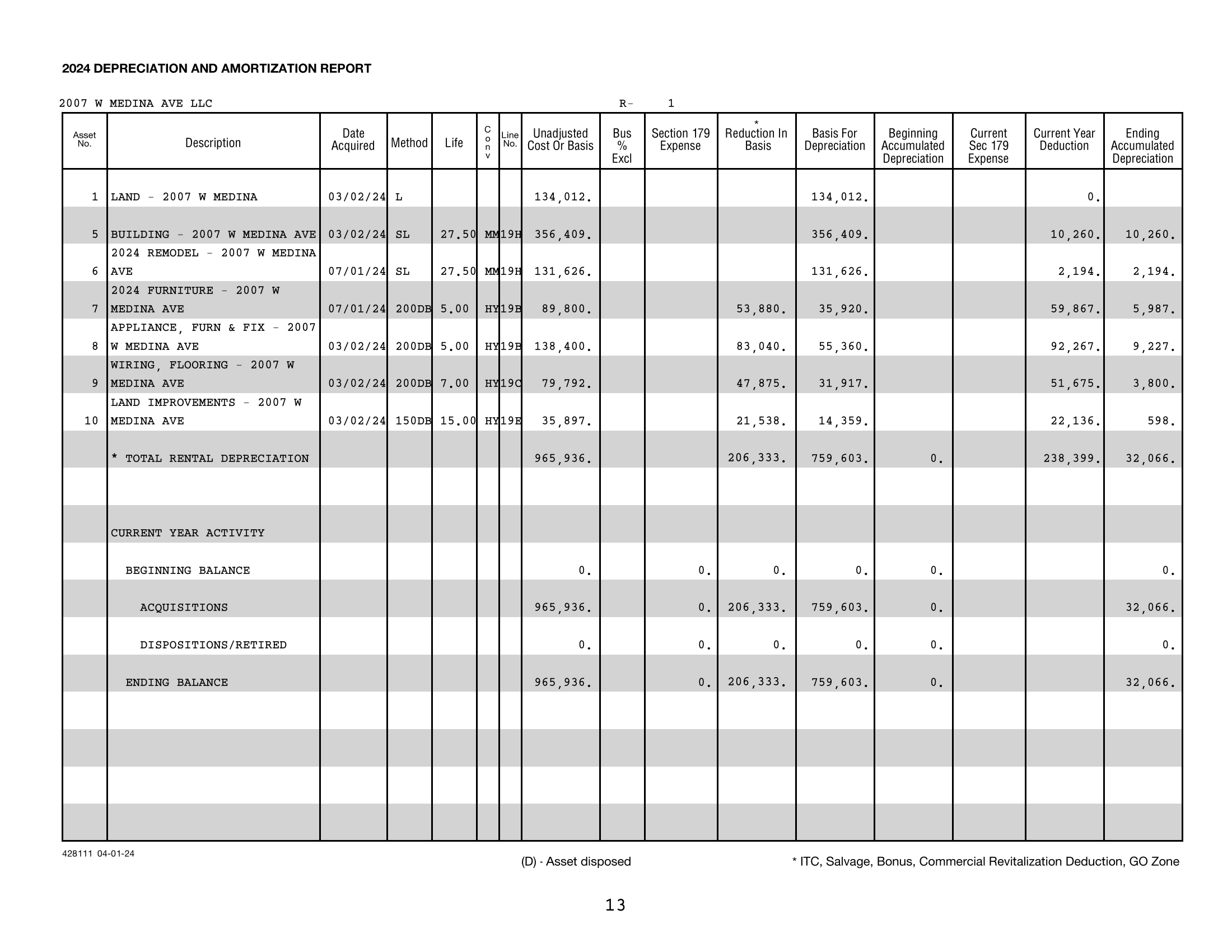

2007 W Medina Ave · Basis waterfall

How a $750,000 house

becomes a $965,936 basis.

Land

$134,012

Building structure (27.5-yr)

$356,409

2024 remodel (27.5-yr)

$131,626

Wiring and flooring (7-yr)

$79,792

Appliances, furniture, fixtures (5-yr)

$138,400

2024 launch furniture (5-yr)

$89,800

Land improvements (15-yr)

$35,897

Total depreciable basis

$965,936

Source · 2007 W Medina Ave LLC · 2024 Form 1065 · Form 4562 Depreciation Report

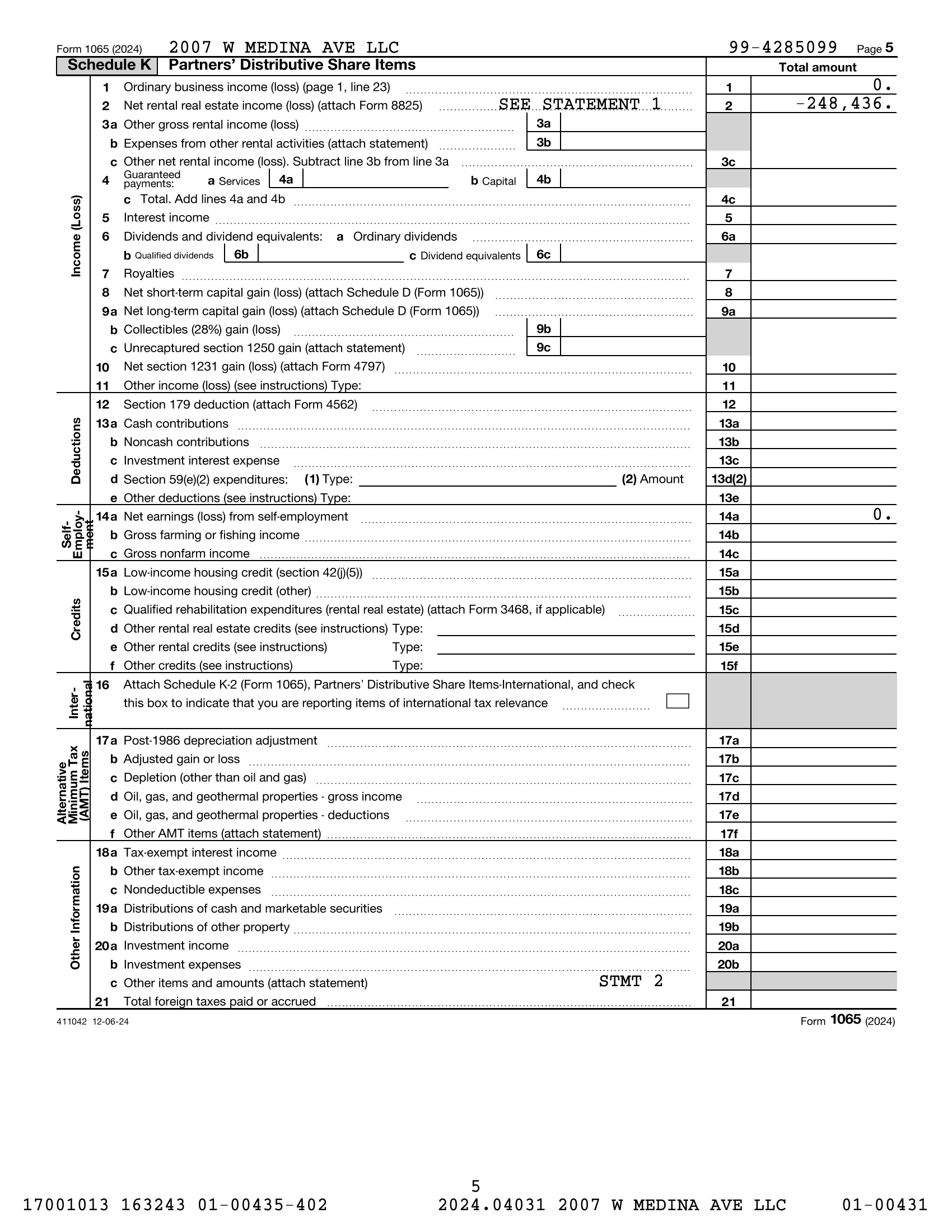

The line item · Schedule K, line 2

This is what shows up

on the K-1.

Source · 2007 W Medina Ave LLC · 2024 Form 1065 · Schedule K, line 2

Net rental real estate loss −$248,436

That single line item is the entire pitch. It is reported on Form 8825, attached to the partnership return, and flows through the K-1 to the owner's personal 1040.

If you materially participate in a short-term rental with average guest stays under seven days, that loss is non-passive. It offsets ordinary income, capital gains, and one-time taxable events on your individual return.